Let me be clear from the start: Quantinuum going public is not evidence that quantum computing has arrived. It is evidence that investors believe it might arrive, eventually, and they want exposure to that possibility before the market prices it in. These are very different things, and the conflation of the two in recent coverage has been frustrating to watch.

That said, I should complicate my own skepticism. Quantinuum is not a typical quantum startup. The company has genuine technical credentials, a clear hardware roadmap, and backing from Honeywell International Inc., which spun out its quantum division to form the company. The decision to boost their IPO target to as much as $1.46 billion (up from earlier estimates, with both the share count and price range increasing) suggests institutional demand is real. So what is actually going on here?

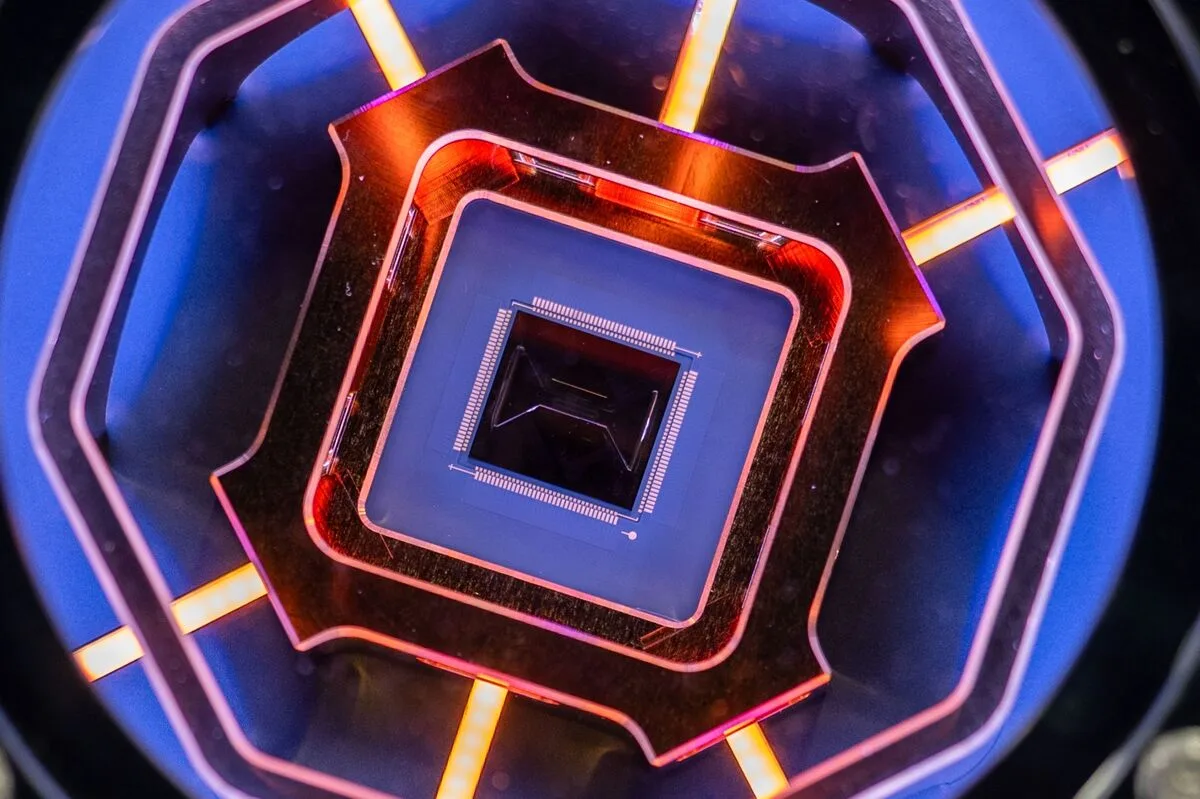

Quantinuum operates trapped-ion quantum computers, which represent one of several competing approaches to building fault-tolerant quantum systems. To be precise, trapped-ion systems have historically demonstrated higher gate fidelities than superconducting qubit systems (the approach favored by IBM and Google), though they have faced challenges with scaling qubit counts and operational speed.

The company's H-Series processors have shown strong performance on certain benchmarks. Their H2 processor, announced in 2024, demonstrated what the company called "record" quantum volume scores. I know I'm being picky here, but quantum volume as a metric has significant limitations: it measures a specific type of circuit depth and doesn't necessarily translate to practical computational advantage for real-world problems.

What's genuinely interesting about Quantinuum's approach is their focus on error correction and their claims about logical qubit performance. In April 2024, the company published results showing they had achieved certain error correction thresholds. However, the path from these demonstrations to commercially useful quantum computation remains unclear, and the company hasn't disclosed precise timelines for when they expect to achieve "quantum advantage" on problems that matter to paying customers.

According to WIRED, Quantinuum is "losing millions" but investors "want in anyway." This pattern is familiar from other deep-tech sectors: the bet is not on current profitability but on future market capture.

The logic, such as it is, runs something like this: quantum computing will eventually transform cryptography, drug discovery, materials science, and optimization problems. Whoever builds the first truly useful quantum computer will capture enormous value. Quantinuum is one of perhaps five to ten serious contenders globally. Therefore, owning a piece of Quantinuum is owning a lottery ticket with better-than-random odds.

I find this reasoning partially compelling and partially concerning. The compelling part is that Quantinuum does have real technology and real expertise. The Honeywell backing provides both capital and credibility. The concerning part is that "eventually" is doing a lot of work in that investment thesis. We don't actually know when (or, to be honest, whether) fault-tolerant quantum computers will achieve practical advantage over classical systems for commercially relevant problems.

The sample size of successful quantum computing IPOs is exactly zero, which makes it difficult to assess whether the market is pricing this correctly. IonQ went public via SPAC in 2021 and has seen its stock price decline substantially from its peaks, though it has recovered somewhat in 2025. That's one data point, and it's not especially encouraging.

The decision to boost the offering to $1.46 billion, as reported by Bloomberg, suggests that initial investor interest exceeded expectations. This is notable because it indicates that institutional investors, who presumably have access to detailed financial projections and technical due diligence, are comfortable with the valuation.

But I want to be careful here. Strong IPO demand does not validate the underlying technology. It validates that investors believe other investors will want to own the stock. These are related but distinct phenomena. The history of technology IPOs includes many examples of companies that raised substantial capital, generated significant investor enthusiasm, and subsequently failed to deliver on their technical promises. (I'm thinking of various cleantech companies from the 2008-2012 period, though the comparison is imperfect.)

What we don't know from the available reporting is the company's actual path to profitability. How much revenue is Quantinuum generating from its current quantum computing services? What is the customer retention rate? What are the unit economics of providing quantum computing access? These details matter enormously for evaluating whether the IPO price makes sense, and I haven't been able to find clear answers in the public coverage.

Quantinuum's IPO comes at an interesting moment for the quantum computing sector. IonQ, which also uses trapped-ion technology, has been public for several years and provides a partial comparison. Google's quantum AI division remains part of Alphabet. IBM continues to develop its superconducting qubit roadmap. Various startups (PsiQuantum, Xanadu, Rigetti) are pursuing different technical approaches with varying levels of funding and progress.

It's worth noting that the competitive landscape remains genuinely uncertain. We don't know which hardware approach will ultimately prove most practical for fault-tolerant quantum computing. Trapped ions have advantages in gate fidelity; superconducting qubits have advantages in speed and, potentially, scaling. Photonic approaches (like PsiQuantum's) have advantages in operating temperature but face challenges in deterministic gate operations.

Quantinuum's bet is that trapped-ion systems will prove superior, or at least competitive, as the field matures. This is a reasonable bet but not a certain one. The honest answer is that nobody knows which approach will win, and anyone who claims otherwise is either overconfident or selling something.

If I were evaluating Quantinuum as a long-term investment (which, to be clear, I am not in a position to do and am not recommending), I would want to see several things that are not currently available in public reporting.

First, I would want detailed benchmarks comparing Quantinuum's systems to competitors on standardized tasks. Not quantum volume, which has limited practical relevance, but performance on specific algorithms that potential customers actually care about: variational quantum eigensolvers for chemistry, quantum approximate optimization for logistics, and so on.

Second, I would want to understand the company's error correction roadmap in more detail. What is the timeline to achieving logical qubits with error rates low enough for practical computation? What are the engineering challenges remaining, and how confident is the team in overcoming them?

Third, I would want to see customer case studies. Who is actually using Quantinuum's systems, for what purposes, and are they deriving value that justifies continued spending? The quantum computing industry has a history of impressive technical demonstrations that don't translate to commercial traction.

None of this is to say that Quantinuum is a bad company or a bad investment. It is to say that the available public information is insufficient to make a confident judgment either way. The IPO price reflects investor enthusiasm, which may or may not be justified by fundamentals that we cannot currently assess.

I've been asked this question many times, and my answer remains frustratingly equivocal: it depends on what you mean by "overhyped."

If you mean "will quantum computers eventually do useful things that classical computers cannot," then probably yes, though the timeline remains unclear and could be decades rather than years.

If you mean "are current quantum computers commercially useful for most applications," then no, not really, with some narrow exceptions in research and certain optimization problems where even noisy intermediate-scale quantum (NISQ) systems provide marginal advantages.

If you mean "are quantum computing company valuations justified by current fundamentals," then almost certainly not, but that's true of many technology sectors where investors are pricing in future potential rather than present performance.

Quantinuum's IPO is, in a sense, a referendum on this last question. Investors are betting that the company will eventually deliver on the promise of quantum computing, and they're willing to pay $1.46 billion for that bet. Whether that bet pays off depends on technical progress that no one, including Quantinuum's own researchers, can guarantee.

I remain skeptical of the timeline and confident that most near-term applications of quantum computing are overstated. But I also recognize that I could be wrong, and that Quantinuum is among the more credible companies working on the problem. The honest position is uncertainty, which is probably not what investors want to hear but is, I think, the correct one.