What does a company that made $60 billion in net income last fiscal year need with a bond sale?

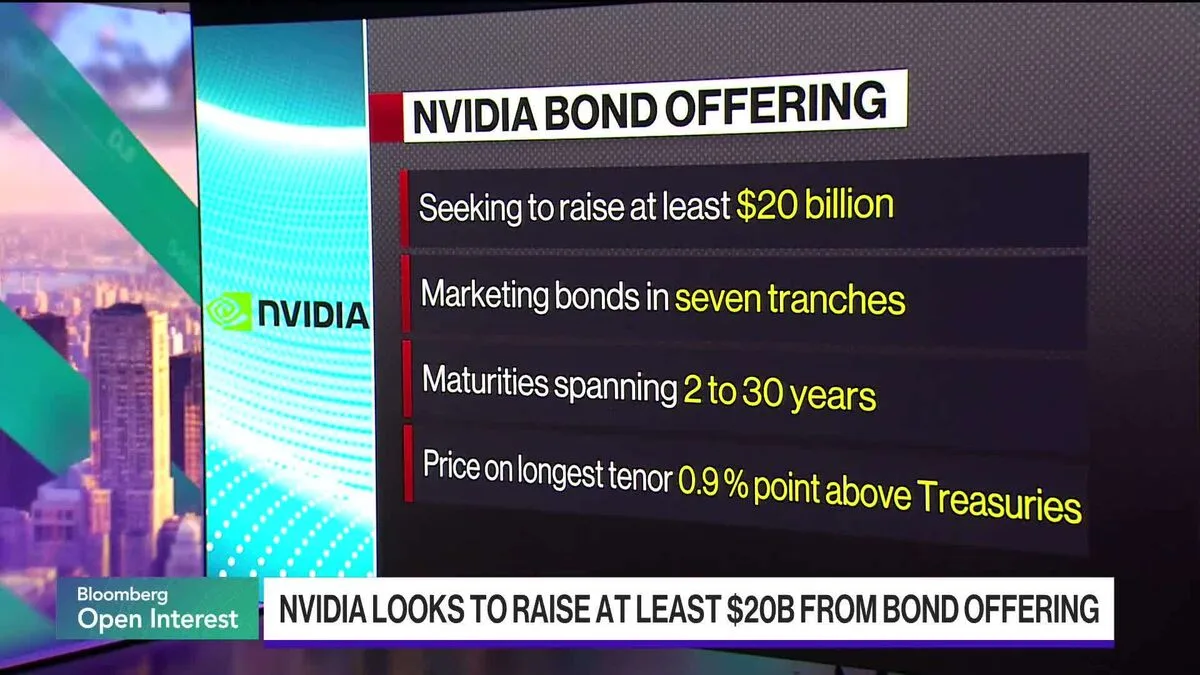

That is the question worth sitting with when you read that Nvidia is preparing to raise at least $20 billion through its first corporate bond sale since 2021. According to people with direct knowledge of the matter, as reported by Bloomberg, the offering is structured across seven tranches with maturities ranging from two to thirty years. Ed Ludlow, covering the story for Bloomberg's markets desk, framed it simply: "Bloomberg Open Interest."

Simple framing for a transaction that is, in context, anything but simple.

To understand why this matters, it helps to understand what Nvidia's balance sheet actually looks like right now. The company has accumulated substantial cash reserves on the back of extraordinary GPU demand driven by large language model training and inference workloads. Its data center segment has been the dominant revenue driver for several consecutive quarters, and analysts have largely treated the stock as a proxy for the broader AI infrastructure buildout.

So, to be precise, the question is not whether Nvidia can afford its capital needs from operating cash flow. It almost certainly can. The question is why it is choosing not to.

Corporate finance has a fairly standard answer to that question: when interest rates allow it and when you have investment-grade credit, issuing debt is often cheaper than deploying equity or cash reserves, particularly if you want to preserve optionality. A seven-tranche structure with maturities out to thirty years is not a company scrambling for liquidity. It is a company locking in long-duration capital at rates it finds acceptable, against a backdrop of investments it expects to take decades to fully pay off.

It is worth noting that Nvidia last went to the bond market in 2021, when it was a much smaller company by revenue and market capitalisation. The scale of this offering, at least $20 billion, reflects how dramatically the business has changed.

The transaction itself is, in narrow financial terms, incremental. Large technology companies issue investment-grade bonds regularly. Apple has done it repeatedly. Microsoft has done it. This is not a novel instrument or a novel strategy.

What is genuinely new is the scale relative to Nvidia's previous bond activity, and what that scale implies about the company's capital planning horizon. A thirty-year tranche is a statement. It says: we expect to be generating enough cash to service this debt comfortably across three decades, and we expect the underlying business to remain durable over that period. That is a significant bet on the longevity of AI infrastructure demand, made explicit in the structure of the offering.

It also raises a more interesting question for those of us who cover research and AI models rather than capital markets: what is this money actually for?

Nvidia has not publicly disclosed the specific intended uses of proceeds beyond the standard language around general corporate purposes. The company didn't disclose exact figures on how capital might be allocated across its various investment priorities. But we can make reasonable inferences from what we know about where Nvidia is spending.

Nvidia's business model has, over the past three years, become inseparable from the infrastructure layer of modern AI. Its H100 and H200 GPUs are the dominant compute substrate for training frontier models, and the upcoming Blackwell architecture is already the subject of intense demand from hyperscalers. The company has also been investing in its software stack (CUDA, NIM microservices, the broader NEMO framework for model development), in networking through Mellanox-derived InfiniBand products, and in what it calls "AI factories," the full-stack data centre configurations it sells to enterprise customers.

All of this requires capital. Not just for manufacturing, which is largely outsourced to TSMC, but for research and development, for acquiring talent and smaller companies, and for building out the kind of systems-level integration work that keeps customers locked into the Nvidia ecosystem.

A $20 billion raise, structured over long maturities, is consistent with a company planning a significant multi-year capital deployment. Whether that is acquisitions, expanded R&D, or investments in its own data centre capacity remains unclear at this point.

What the bond sale does signal, fairly clearly, is that Nvidia's leadership believes the current AI infrastructure cycle is not a short-term phenomenon. You do not issue thirty-year debt against a business you think might plateau in five years. That is a structural bet on sustained demand, and it is worth taking seriously as a data point even if you are skeptical of some of the more breathless projections about AI adoption curves.

(I am, for the record, somewhat skeptical of those projections. But Nvidia's CFO team has access to order books and customer conversations that public analysts do not, and their revealed preference here is informative.)

There is a broader point here that I think gets underappreciated in coverage of AI companies, which tends to focus on product launches, benchmark results, and stock performance. The debt capital markets are, in some ways, a more sober signal of long-term confidence than equity markets.

Equity investors can be, and often are, wrong in both directions. They price in narratives and momentum as much as fundamentals. Bond investors, particularly institutional buyers of investment-grade paper, are doing a different kind of analysis. They are asking: will this company be able to service its obligations across the maturity of this instrument? For a thirty-year tranche, that is a question about business durability, not just the current cycle.

The fact that Nvidia can market a transaction of this size, across seven tranches, with apparent institutional demand, tells us something about how sophisticated fixed-income investors view the company's long-term prospects. It does not tell us they are right. But it is a data point that is harder to dismiss than, say, a bullish equity analyst note.

Actually, the research on this is worth engaging with more carefully. There is a reasonable literature in corporate finance on the informational content of debt issuance decisions, going back to work on pecking order theory and signalling models. The short version: managers with private information about future cash flows tend to prefer debt to equity when they believe the company is undervalued or when they have high confidence in future earnings. A large, long-duration bond offering from a company with Nvidia's cash position is consistent with high internal confidence in the forward earnings trajectory.

I know I am being picky here, but it is worth distinguishing between "Nvidia issued bonds" and "Nvidia issued $20 billion in bonds with thirty-year tranches." The latter is a much stronger signal.

Several things remain genuinely unclear, and I want to be honest about the limits of what we can infer from publicly available information.

First, we do not know the specific use of proceeds. General corporate purposes is a legal disclosure category, not an investment thesis. If Nvidia uses this capital primarily for share buybacks, that is a very different story than if it is funding a major acquisition or a new internal compute buildout.

Second, the timing relative to interest rates matters and is not fully legible from the outside. Nvidia may be issuing now simply because the rate environment is favourable relative to what it expects in 12 to 24 months. That would be a tactical financial decision, not a strategic signal about AI infrastructure at all.

Third, and this is the question I find most interesting from a research standpoint: what does Nvidia's capital allocation tell us about where it thinks the compute bottlenecks will be in three to five years? If the company is investing heavily in networking and systems integration, that suggests it sees interconnect and memory bandwidth as the binding constraints on next-generation AI workloads, which is consistent with what a number of researchers (including work coming out of groups at Stanford and MIT on distributed training efficiency) have been arguing. If the capital goes toward manufacturing partnerships or new fab relationships, that suggests a different view of where the supply chain risks are.

We simply do not know yet. And any analysis that claims to know is working from inference, not disclosed information.

For those of us trying to track the actual trajectory of AI infrastructure investment, a few things would sharpen the picture considerably.

A breakdown of use of proceeds, even at a high level, would be genuinely informative. Nvidia's investor relations team is under no obligation to provide this, but it would help analysts and researchers understand where the company sees its next major capital requirements.

Quarterly data on R&D spending as a percentage of revenue would also be useful. Nvidia's R&D investment has grown in absolute terms but the company's revenue has grown faster, meaning R&D as a share of revenue has actually declined over the past two years. If this bond capital is going toward R&D expansion, that ratio should shift. If it does not, that tells us something about priorities.

Finally, and this is more of a wish than an expectation, some transparency about what Nvidia is funding in terms of fundamental research versus applied engineering would help the broader research community understand where the company sees the unsolved problems. The gap between what Nvidia's internal researchers are working on and what is being published is, based on what I can track through arXiv and conference proceedings, substantial and growing.

For now, what we have is a $20 billion bond offering, a seven-tranche structure, maturities out to thirty years, and a company that is clearly planning for a very long run. Whether that planning reflects genuine foresight about AI's infrastructure needs, or whether it is sophisticated financial engineering against a business cycle that will eventually turn, is a question this transaction alone cannot answer.

But it is the right question to keep asking.