Micron's $1 Trillion Milestone Signals Memory's Central Role in AI Infrastructure

The chipmaker's valuation surge reflects a broader shift in how we think about AI hardware bottlenecks, though the fundamentals deserve closer scrutiny.

画像クレジット: Image via source article. Used under fair use for news commentary. · source

Let me be clear about something upfront: Micron crossing the $1 trillion valuation threshold is not, in itself, a technical achievement. It is a market event. But it is a market event that tells us something genuinely interesting about where the AI hardware stack is heading, and why memory, long treated as a commodity afterthought, is suddenly commanding attention.

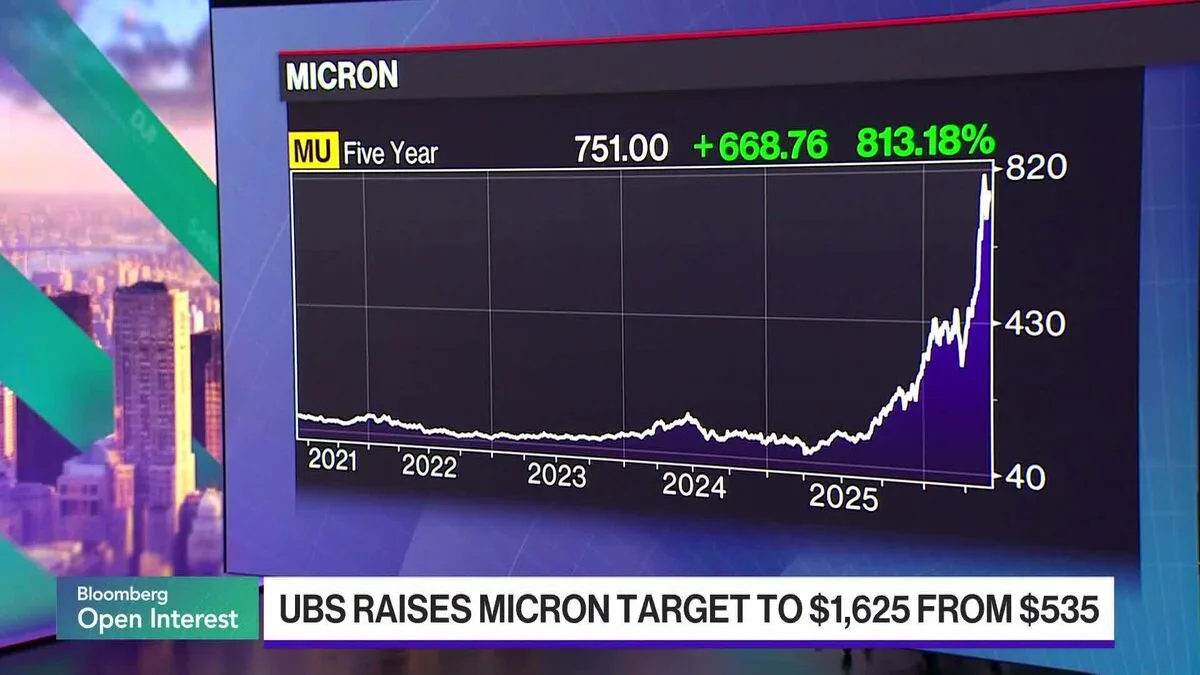

The numbers are striking. UBS recently raised its price target on Micron to $1,625, up from $535, representing a Street-high view that would have seemed almost absurd two years ago. And yet here we are, with the company reportedly trading at under 10 times forward earnings despite the trillion-dollar milestone. That valuation gap, the disconnect between market cap and earnings multiple, is worth examining.

For years, discussions about AI hardware focused almost exclusively on compute. GPUs, TPUs, custom ASICs. The assumption, sometimes stated explicitly and sometimes just baked into how people talked about the field, was that memory would scale alongside compute without becoming a limiting factor. This assumption, it's worth noting, was always a bit optimistic.

The problem is straightforward in principle, though the engineering details get complicated quickly. Large language models and their successors require not just fast computation but fast access to enormous parameter sets. When your model has hundreds of billions of parameters, the time spent moving data between memory and compute can dominate the time spent actually doing matrix multiplications. This is the memory wall, and it has been a known issue in computer architecture for decades.

関連記事

More in AI Models

Chipmakers swung wildly this week, from a Tuesday 'chip-wreck' to a Micron-led surge after hours. What's actually going on with AI's hardware backbone?

Sarah Williams · 26 Jun · 5 min

The original Creator Studio was shut down in 2023. Now it's back, rebuilt around an AI assistant that promises to grow your audience and reply to comments in your voice.

Sarah Williams · 26 Jun · 5 min

At its annual Config conference, Figma announced coding layers, AI-generated motion graphics, and a reimagined canvas that blurs the line between design and full-stack development.

Sarah Williams · 26 Jun · 5 min

Everyone talks about chips and models. The memory bottleneck is the part of the AI buildout that keeps getting underestimated, and Micron's latest earnings make that case hard to ignore.

What has changed is the scale. Training runs that cost hundreds of millions of dollars are now memory-constrained in ways that matter economically. Inference at scale, serving millions of queries against large models, faces similar constraints. High-bandwidth memory (HBM) has become the critical path.

I should be precise here about what Micron's market surge does and does not indicate. It reflects investor confidence that demand for high-bandwidth memory will continue to outstrip supply for the foreseeable future. It reflects expectations that Micron's HBM3E and future products will capture significant share of that demand. It reflects, in short, a bet on the memory bottleneck thesis.

What it does not necessarily reflect is any particular technical breakthrough. Micron has been executing well on HBM manufacturing, but the underlying technology is not dramatically different from what the company and its competitors have been developing for years. This is incremental improvement at scale, not a paradigm shift. (I know I'm being picky here, but the distinction matters when we're trying to understand what's actually happening in the technology versus what's happening in the market.)

The valuation also carries assumptions about competitive dynamics that may or may not hold. Samsung and SK Hynix are not standing still. The memory market has historically been brutally cyclical, with periods of oversupply crushing margins. Whether the current demand environment represents a structural shift or a particularly extended cycle remains, honestly, unclear.

For those of us who follow robotics and embodied AI, Micron's trajectory matters for reasons that go beyond general AI infrastructure trends. The computational demands of robotics are evolving in ways that will make memory architecture increasingly relevant.

Consider the shift toward foundation models for robotics. Systems like RT-2, PaLM-E, and their successors are attempting to bring the benefits of large-scale pretraining to physical manipulation and navigation. These models are enormous. Running them in real-time on edge hardware, the kind of hardware that actually fits on a robot, requires aggressive optimization of memory bandwidth.

The latency constraints are also different from cloud inference. When a robot arm is moving toward an object, you cannot afford the kind of batching strategies that make large model inference efficient in data centers. You need fast, single-query responses. This pushes the memory bottleneck in directions that the broader AI infrastructure conversation sometimes overlooks.

There's also the question of on-robot learning. Systems that adapt to their environments in real-time, updating world models or policy networks based on recent experience, need to write to memory as well as read from it. The read/write asymmetries in different memory technologies become relevant here in ways they might not for pure inference workloads.

I want to return to that striking detail: trading at under 10 times forward earnings despite a trillion-dollar market cap. This suggests one of several things.

First, it could indicate that earnings expectations are extremely high. If the market believes Micron will generate $100+ billion in forward earnings, then the multiple is not actually that compressed. This would imply expectations of sustained, extraordinary demand that some analysts might find optimistic.

Second, it could indicate that the market is pricing in significant risk. Cyclicality, competition, potential demand destruction if AI scaling hits unexpected walls. A low multiple on high expected earnings can reflect uncertainty about whether those earnings will actually materialize.

Third, it could indicate that the market is simply not yet fully pricing in the AI memory thesis. That the trillion-dollar valuation, impressive as it sounds, actually undervalues the company relative to its future cash flows. This is, to be clear, the bull case.

I do not have strong conviction about which of these interpretations is correct. The honest answer is that predicting memory market dynamics over multi-year horizons is difficult, and anyone who claims certainty is probably overconfident.

Several things remain unclear to me, and I think they should remain unclear to anyone being intellectually honest about this space.

First, how durable is the current demand environment? AI training and inference demand has been growing faster than most predictions, but extrapolating exponential growth indefinitely is a classic forecasting error. At some point, either the applications plateau, the efficiency improvements catch up, or the economics stop working. When that happens, and whether it happens in two years or ten, matters enormously for memory company valuations.

Second, what does the competitive landscape look like in HBM specifically? Micron has been gaining share, but this is a three-player market (with Samsung and SK Hynix), and all three are investing heavily. The barriers to entry are high, but they're not infinite, and the Chinese semiconductor industry is working aggressively on memory technologies despite export controls.

Third, how do alternative architectures affect the picture? There's active research on in-memory computing, neuromorphic approaches, and other paradigms that could change the memory/compute relationship. Most of this is still in the research phase, and I would not bet on any particular alternative displacing conventional architectures in the near term. But over a decade? The technical landscape could look quite different.

If I were advising Micron (I'm not, and they probably don't need my advice given their current trajectory), I would want to see more engagement with the robotics and embodied AI community specifically.

The edge inference problem for robotics is different enough from cloud inference that it deserves dedicated attention. Memory solutions optimized for the latency profiles, power constraints, and form factors of robotic systems could be a meaningful differentiation point. The volumes are smaller than data center, obviously, but the margins could be attractive and the technical challenges are interesting.

I would also want to see more transparency about manufacturing capacity and yield. The memory industry has a history of supply announcements that turn out to be optimistic. Understanding how much HBM capacity is actually coming online, and at what cost curves, would help the market (and researchers) make better decisions.

Finally, I would want to see more published research on the memory requirements of specific AI workloads. Micron has the data on what their customers are actually doing with high-bandwidth memory. Sharing more of that information, in appropriately anonymized form, would benefit the broader research community and might help identify bottlenecks that the company could address.

Micron's trillion-dollar milestone is, in one sense, just a number. Market capitalizations fluctuate. Price targets get revised up and down. The semiconductor industry has seen cycles of euphoria and despair before.

But in another sense, it represents something real: a recognition that memory has moved from supporting actor to co-star in the AI hardware story. The companies that can manufacture high-bandwidth memory at scale, with good yields, at competitive prices, are going to be critical infrastructure providers for the next phase of AI development.

For robotics specifically, this matters because the field is increasingly dependent on large models that push memory constraints. The foundation model approach to robotics, whatever you think of its ultimate potential, requires the kind of memory bandwidth that only a few companies in the world can provide. Micron is one of them.

Whether the current valuation is justified, whether the demand will persist, whether competitors will catch up, these are questions I cannot answer with confidence. But the underlying technical trend, memory as a critical bottleneck for AI systems including robotic ones, seems durable. That, at least, is worth paying attention to.