Oracle's AI Infrastructure Story Is Solid. The Market Just Doesn't Know What to Do With It.

Strong earnings, lukewarm reaction. Bob Macintosh thinks the Oracle situation tells you something useful about where AI infrastructure hype meets hard numbers.

Crédit photo: Image via Bloomberg — Technology. Used under fair use for news commentary. · source

Picture a warehouse floor in the mid-2000s. Big Oracle database humming away in a back room, nobody glamorous talking about it, nobody putting it on a conference keynote slide. It just worked. Procurement ran on it. Inventory ran on it. Half the plant floor data ended up in it eventually.

That image came back to me this week when Oracle dropped its Q4 earnings and the market basically shrugged.

Look, here's the thing. The numbers weren't bad. By most reads, they were actually pretty good. Rishi Jaluria over at RBC Capital Markets called them "really strong" on Bloomberg, and his read was that Oracle is functioning as a kind of proxy for the broader AI infrastructure buildout trade right now. Cloud demand up, AI-related contracts growing. That's not nothing.

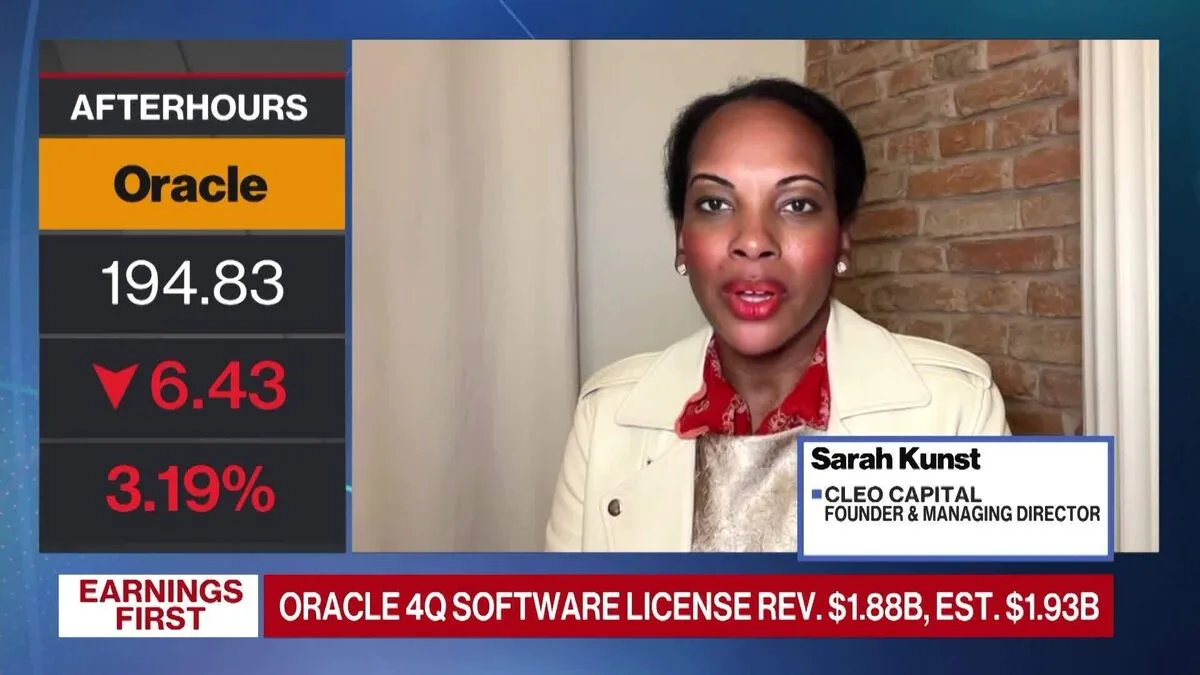

But Sarah Kunst at Cleo Capital put it more bluntly on "Bloomberg The Close," saying the bloom is off the rose for Oracle and she's not shocked investors aren't excited. And honestly, I think both of them are right, which is the mildly annoying part.

Strong Numbers, Weak Story

The problem Oracle has isn't the business. The problem is narrative positioning. When I was at Kuka, we'd sometimes deliver a project on spec, on time, under budget, and the customer would still be vaguely disappointed because their expectations had drifted somewhere unrealistic during the sales process. Oracle feels a bit like that right now. The AI infrastructure buildout is genuinely happening. Oracle's cloud and GPU capacity plays are real. But the story investors wanted was something flashier, something with a sharper edge.

À lire aussi

More in Industrial

The Apple supplier priced its shares at the maximum and still had to turn away demand, which tells you something about where hardware money is flowing right now.

James Chen · 25 Jun · 5 min

Prime Day deals on Echos and Ring cameras are fine, but let's not confuse consumer gadgets with the serious robotics work happening in warehouses.

Robert "Bob" Macintosh · 25 Jun · 3 min

Amazon's CEO made his first India trip and left behind a $13 billion AI commitment and an aggressive quick-commerce expansion. The numbers are real. The execution is the hard part.

James Chen · 25 Jun · 6 min

A wave of arXiv preprints this week tackles one of manipulation's oldest problems: how do you get a robot to learn from imperfect, incomplete, or just plain missing data?