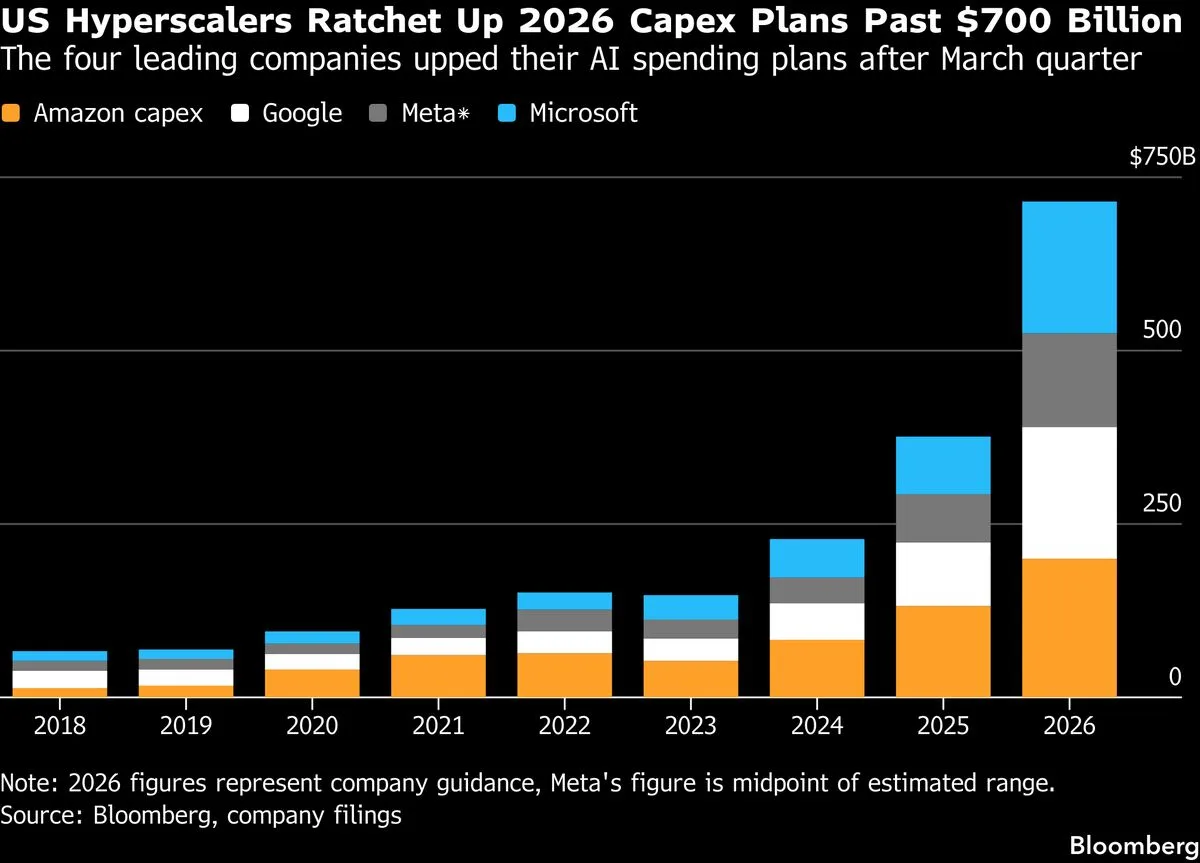

Image credit: Image via Bloomberg — Technology. Used under fair use for news commentary. · source

Most of the coverage that came out on June 9th treated China's 2 trillion yuan AI infrastructure plan as a straightforward geopolitical story. Beijing wants to beat Washington. Big numbers were cited. Analysts weighed in on the tech cold war. And then the news cycle moved on.

What got missed, or at least seriously underweighted, is what this level of sustained compute investment actually means for AI research output, specifically for the kind of large-scale model training and robotics foundation model work that my beat covers. The $295 billion figure is not just a political statement. It is, potentially, a structural shift in who gets to do frontier AI research at scale.

Let me be precise about what is actually being proposed. According to reporting by Bloomberg, China is preparing to spend approximately 2 trillion yuan over the next five years on building data centers across the country. This is a nationwide buildout, not a single facility or cluster. The framing from Beijing is explicitly about propelling the domestic AI sector and surpassing the US. The five-year timeline maps reasonably well onto the current generation of large model development cycles, which is not a coincidence.

To be clear about what we do not know: the full allocation breakdown has not been disclosed publicly, so it remains unclear how much of this capital flows toward training infrastructure versus inference, toward civilian research versus state-directed applications, or toward robotics-adjacent workloads versus general language model development. The company, or in this case the government, did not disclose those figures. That matters for interpreting what this means for any specific research domain.

Related coverage

More in AI Models

Chipmakers swung wildly this week, from a Tuesday 'chip-wreck' to a Micron-led surge after hours. What's actually going on with AI's hardware backbone?

Sarah Williams · 26 Jun · 5 min

The original Creator Studio was shut down in 2023. Now it's back, rebuilt around an AI assistant that promises to grow your audience and reply to comments in your voice.

Sarah Williams · 26 Jun · 5 min

At its annual Config conference, Figma announced coding layers, AI-generated motion graphics, and a reimagined canvas that blurs the line between design and full-stack development.

Sarah Williams · 26 Jun · 5 min

Everyone talks about chips and models. The memory bottleneck is the part of the AI buildout that keeps getting underestimated, and Micron's latest earnings make that case hard to ignore.

Here is where I want to push back on a framing I see a lot in generalist tech coverage: the idea that compute is just one input among many, and that clever algorithms can compensate for hardware disadvantages. This was a reasonable position in 2019. It is considerably less defensible now.

The research literature is fairly unambiguous on this point. The scaling hypothesis, formalized most influentially in the work coming out of OpenAI and DeepMind over the past several years, suggests that for a wide class of tasks, performance improvements track reliably with increases in compute, data, and parameters. Chinchilla scaling laws (Hoffmann et al., 2022) refined our understanding of the optimal compute-to-data ratio, but did not overturn the fundamental relationship. More compute, trained intelligently, produces better models.

For robotics specifically, the implications are significant. The recent wave of robotics foundation models, things like RT-2 from Google DeepMind, or the various efforts to apply vision-language-action architectures to manipulation tasks, are all deeply compute-hungry. Training a model that can generalize across robot morphologies and task types requires enormous amounts of diverse demonstration data processed through very large networks. You cannot do that on a laptop. You cannot do it on a small cluster. You need the kind of sustained, large-scale infrastructure that China is now explicitly committing to build.

It is worth noting that China's domestic robotics research output has already been growing substantially. If you track publications at venues like ICRA, IROS, and CoRL over the past five years, the proportion of China-affiliated first authors has increased considerably. I am not going to put a precise number on that because I have not done a rigorous systematic review of the citation data, and I would rather flag the uncertainty than overstate the case. But the directional trend is not in dispute.

The key points worth holding in mind as this story develops:

The 2 trillion yuan figure covers five years, which means roughly 400 billion yuan per year, or around $59 billion annually at current exchange rates. For context, that is a significant fraction of the total global hyperscale data center capital expenditure in recent years.

The buildout is described as nationwide, suggesting distributed infrastructure rather than a single concentrated cluster. This has implications for latency, redundancy, and the kinds of workloads that can be efficiently run.

Beijing's explicit framing around surpassing the US positions this as a long-term strategic commitment, not a one-time stimulus. Sustained political will behind infrastructure spending tends to be more durable than market-driven cycles.

The timeline overlaps with what many researchers expect to be a critical period for embodied AI and robotics foundation models. The next three to five years are widely considered formative for whether general-purpose robot manipulation becomes tractable.

Export controls on advanced semiconductors from the US side create a genuine constraint on China's ability to access the most capable training hardware. How the buildout navigates that constraint, through domestic chip development, stockpiling, or architectural workarounds, is genuinely unclear.

That last point deserves more attention than it usually gets. The Huawei Ascend line and various domestic alternatives to Nvidia's H100 and subsequent chips are real products, but the performance gap is not trivial. I know I am being picky here, but the distinction between having a lot of compute and having a lot of competitive compute matters enormously for whether this investment translates into frontier model capabilities or into a very large but somewhat behind-the-frontier infrastructure base.

There is a version of this story where the $295 billion plan is mostly noise, a political commitment that gets partially implemented, produces a lot of data centers running workloads well below their theoretical capacity, and does not materially change the competitive landscape in AI research. That version is possible.

There is another version where this represents the kind of sustained, state-backed infrastructure investment that genuinely shifts where frontier research happens. Academic and industrial researchers follow compute. If Chinese institutions can offer access to large-scale training infrastructure that is genuinely competitive, the gravitational pull on talent and research direction is real.

Actually, the research shows a pattern here that is worth taking seriously. The US dominance in AI research over the past decade was not purely a function of intellectual culture or university quality. It was substantially a function of the fact that the compute was here, at Google, Microsoft, Meta, and Amazon, and researchers who wanted to work at scale needed to be affiliated with those institutions or their partners. That structural advantage is not permanent.

For robotics AI specifically, this raises questions about, well, multiple things: where the next generation of foundation models gets trained, which institutions get early access to the resulting capabilities, and whether the current assumption that US-based labs will set the research agenda for embodied AI holds through the end of this decade.

I want to be careful not to overread a single policy announcement. This is based on Bloomberg's reporting of a plan that is still being prepared, not a fully implemented program. Plans change. Funding gets redirected. Five-year projections in any domain carry substantial uncertainty, and five-year projections for a technology sector moving as fast as AI carry more uncertainty than most.

But the direction is clear enough to warrant serious attention from anyone working in or adjacent to this field. The assumption that frontier AI research is primarily a US and European endeavor, with China as a fast follower, seems increasingly worth questioning.

If I were designing the follow-up coverage on this story, the questions I would want answered are fairly specific. First, what is the semiconductor procurement strategy? The export control environment means that the effective compute capacity of this infrastructure depends heavily on what hardware actually gets deployed. Second, how much of this is directed toward specific research programs versus general-purpose commercial cloud capacity? Those are very different things with very different implications for research output. Third, what are the energy infrastructure commitments that accompany this? Data centers at this scale require sustained power delivery, and the locations chosen for the buildout will reflect both grid capacity and cooling constraints.

None of those questions have clear public answers right now. The reporting we have is, in a way, the headline number and the strategic framing. The operational details that would let us assess whether this translates into genuine research capability remain opaque.

That opacity is itself worth noting. It makes confident claims in either direction, that this definitely will or definitely will not reshape the AI research landscape, premature. What it does do is establish a clear prior: when a government commits $295 billion to infrastructure over five years, the null hypothesis that nothing changes is probably not the right starting point.